IN THE SPOTLIGHT

Manasquan Bank’s Ralph Tancredi Sr. Recognized in Scotsman Guide and National Mortgage News Rankings

WALL TOWNSHIP, NJ (May 14, 2026) - Ralph G. Tancredi, Sr., SVP, Residential Lending Sales Manager for Manasquan Bank, has been nationally recognized for the tenth consecutive year as a top-performing mortgage professional, earning distinction from both National Mortgage News and Scotsman Guide, based on 2025 residential loan closing volume.

Little Egg Harbor Shred Day, May 9th

Save the date! Clear the clutter, for free. Just bring your papers and we’ll do the shredding and recycling. You leave with one item checked off your to-do list. The event is set to wrap up at 10:30am but is subject to end earlier if the truck is full.

A Day in the Life at Jenkinson’s: Community, Connection & Carousel Rides with Manasquan Bank

What happens when you step away from the desk and onto the boardwalk? In this episode of On the Clock, Manasquan Bank Chair, President & CEO Jim Vaccaro heads to Jenkinson’s Boardwalk in Point Pleasant to experience a day in the life of one of the bank’s valued commercial business clients.

Manasquan Bank Champions Neuroinclusive Living as Sole Institutional Lender for THRIVE Red Bank

In a powerful display of mission-driven community investment, Manasquan Bank proudly served as the sole institutional lender for THRIVE Red Bank, a visionary neuroinclusive housing development that officially broke ground on Wednesday, July 30th at 273 Shrewsbury Avenue. Bank executives were on-site to support the ribbon-cutting ceremony, celebrating the start of a development that will offer life-changing opportunities for neurodivergent adults and serve as a model for inclusive living.

Community Day 2025 + Annual Days of Giving

We're Gonna Need a Bigger Plaza! Get ready to make a splash—our 2025 Community Day is circling closer, and this year’s theme is JAWS! Whether you're a fan of finned friends or just love bringing the community together, you won’t want to miss this unforgettable event filled with family fun, food, games, and a whole lot of heart.

What Are You Interested In Today?

Press Releases

Manasquan Bank’s Ralph Tancredi Sr. Recognized in Scotsman Guide and National Mortgage News Rankings

WALL TOWNSHIP, NJ (May 14, 2026) - Ralph G. Tancredi, Sr., SVP, Residential Lending Sales Manager for Manasquan Bank, has been nationally recognized for the tenth consecutive year as a top-performing mortgage professional, earning distinction from both National Mortgage News and Scotsman Guide, based on 2025 residential loan closing volume.

Manasquan Bank’s James S. Vaccaro Appointed President of National Community Depository Institutions Advisory Council (CDIAC)

WALL TOWNSHIP, NJ (March 9, 2026) - Manasquan Bank is proud to announce that its Chair, President, and CEO, James S. Vaccaro, has been appointed President of the National Community Depository Institutions Advisory Council (CDIAC) for the year 2026. The appointment was confirmed by Michelle W. Bowman, Vice Chair for Supervision of the Board of Governors of the Federal Reserve System.

Manasquan Bank Team Recognized in Scotsman Guide and National Mortgage News Rankings

WALL TOWNSHIP, NJ (December 23, 2025) - Ralph G. Tancredi, Sr., SVP, Residential Lending Sales Manager for Manasquan Bank, has been nationally recognized for the ninth consecutive year as a top-performing mortgage professional, earning distinction from both National Mortgage News and Scotsman Guide based on 2024 residential loan closing volume.

Manasquan Bank’s Ralph Tancredi Sr. Recognized in Scotsman Guide and National Mortgage News Rankings

WALL TOWNSHIP, NJ (May 14, 2026) - Ralph G. Tancredi, Sr., SVP, Residential Lending Sales Manager for Manasquan Bank, has been nationally recognized for the tenth consecutive year as a top-performing mortgage professional, earning distinction from both National Mortgage News and Scotsman Guide, based on 2025 residential loan closing volume.

Manasquan Bank’s James S. Vaccaro Appointed President of National Community Depository Institutions Advisory Council (CDIAC)

WALL TOWNSHIP, NJ (March 9, 2026) - Manasquan Bank is proud to announce that its Chair, President, and CEO, James S. Vaccaro, has been appointed President of the National Community Depository Institutions Advisory Council (CDIAC) for the year 2026. The appointment was confirmed by Michelle W. Bowman, Vice Chair for Supervision of the Board of Governors of the Federal Reserve System.

Manasquan Bank Team Recognized in Scotsman Guide and National Mortgage News Rankings

WALL TOWNSHIP, NJ (December 23, 2025) - Ralph G. Tancredi, Sr., SVP, Residential Lending Sales Manager for Manasquan Bank, has been nationally recognized for the ninth consecutive year as a top-performing mortgage professional, earning distinction from both National Mortgage News and Scotsman Guide based on 2024 residential loan closing volume.

Events

Little Egg Harbor Shred Day, May 9th

Save the date! Clear the clutter, for free. Just bring your papers and we’ll do the shredding and recycling. You leave with one item checked off your to-do list. The event is set to wrap up at 10:30am but is subject to end earlier if the truck is full.

Landmark Shred Day, April 11th

Save the date! Clear the clutter, for free. Just bring your papers and we’ll do the shredding and recycling. You leave with one item checked off your to-do list. The event is set to wrap up at 10:30am but is subject to end earlier if the truck is full.

Little Egg Harbor Shred Day, May 9th

Save the date! Clear the clutter, for free. Just bring your papers and we’ll do the shredding and recycling. You leave with one item checked off your to-do list. The event is set to wrap up at 10:30am but is subject to end earlier if the truck is full.

Landmark Shred Day, April 11th

Save the date! Clear the clutter, for free. Just bring your papers and we’ll do the shredding and recycling. You leave with one item checked off your to-do list. The event is set to wrap up at 10:30am but is subject to end earlier if the truck is full.

Blog

A Day in the Life at Jenkinson’s: Community, Connection & Carousel Rides with Manasquan Bank

What happens when you step away from the desk and onto the boardwalk? In this episode of On the Clock, Manasquan Bank Chair, President & CEO Jim Vaccaro heads to Jenkinson’s Boardwalk in Point Pleasant to experience a day in the life of one of the bank’s valued commercial business clients.

We’re Updating Our Fees—Here’s What’s Changing (and What’s Going Away!)

At Manasquan Bank, we’re always looking for ways to enhance your banking experience while staying competitive and aligned with industry standards. After a thorough review of current market trends, operational costs, and service demand, we’re making some important updates to our Consumer and Business Account-Related Fees, effective May 1, 2025.

We’re proud to share that many of our most-used services are now more affordable—or completely free.

Random Act of Kindness Day

Kindness is contagious, and what better way to celebrate Random Acts of Kindness Day on February 17 than with a special giveaway! 🎉 From Monday, February 17, 2025, to Wednesday, February 19, 2025, you and a friend could each win a Hatch Alarm Clock—because everyone deserves a brighter morning! ☀️⏰

That’s it! One lucky winner AND the friend they tagged will both take home a Hatch Alarm Clock. 🎉

Let’s celebrate Random Acts of Kindness Day together and make the world a little brighter—one compliment at a time! 💕 Who will you uplift today?

A Day in the Life at Jenkinson’s: Community, Connection & Carousel Rides with Manasquan Bank

What happens when you step away from the desk and onto the boardwalk? In this episode of On the Clock, Manasquan Bank Chair, President & CEO Jim Vaccaro heads to Jenkinson’s Boardwalk in Point Pleasant to experience a day in the life of one of the bank’s valued commercial business clients.

We’re Updating Our Fees—Here’s What’s Changing (and What’s Going Away!)

At Manasquan Bank, we’re always looking for ways to enhance your banking experience while staying competitive and aligned with industry standards. After a thorough review of current market trends, operational costs, and service demand, we’re making some important updates to our Consumer and Business Account-Related Fees, effective May 1, 2025.

We’re proud to share that many of our most-used services are now more affordable—or completely free.

Random Act of Kindness Day

Kindness is contagious, and what better way to celebrate Random Acts of Kindness Day on February 17 than with a special giveaway! 🎉 From Monday, February 17, 2025, to Wednesday, February 19, 2025, you and a friend could each win a Hatch Alarm Clock—because everyone deserves a brighter morning! ☀️⏰

That’s it! One lucky winner AND the friend they tagged will both take home a Hatch Alarm Clock. 🎉

Let’s celebrate Random Acts of Kindness Day together and make the world a little brighter—one compliment at a time! 💕 Who will you uplift today?

Videos

A Day in the Life at Jenkinson’s: Community, Connection & Carousel Rides with Manasquan Bank

What happens when you step away from the desk and onto the boardwalk? In this episode of On the Clock, Manasquan Bank Chair, President & CEO Jim Vaccaro heads to Jenkinson’s Boardwalk in Point Pleasant to experience a day in the life of one of the bank’s valued commercial business clients.

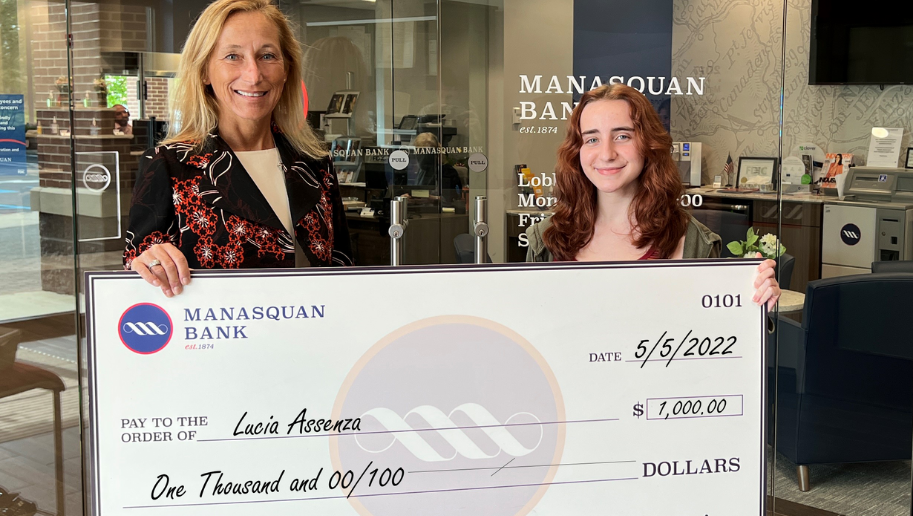

Manasquan Bank Awards Lights, Camera, Save! Local Winner with $1,000

Manasquan Bank’s Lights, Camera, Save! local winner, Lucia Assenza, Marlboro, NJ, was named a national finalist by the American Bankers Association Foundation. Lights, Camera, Save! is an annual video contest that encourages teens ages 13-18 to produce a short, 30-second film that communicates the importance of sound financial habits.

A Day in the Life at Jenkinson’s: Community, Connection & Carousel Rides with Manasquan Bank

What happens when you step away from the desk and onto the boardwalk? In this episode of On the Clock, Manasquan Bank Chair, President & CEO Jim Vaccaro heads to Jenkinson’s Boardwalk in Point Pleasant to experience a day in the life of one of the bank’s valued commercial business clients.

Manasquan Bank Awards Lights, Camera, Save! Local Winner with $1,000

Manasquan Bank’s Lights, Camera, Save! local winner, Lucia Assenza, Marlboro, NJ, was named a national finalist by the American Bankers Association Foundation. Lights, Camera, Save! is an annual video contest that encourages teens ages 13-18 to produce a short, 30-second film that communicates the importance of sound financial habits.

Get to know your bank better today! Choose your topic of interest to watch videos, listen to podcasts, and browse articles. Our digital resources are created to serve the needs of our individual clients and the greater banking community.

Social MediaStay Tied Together with Manasquan Bank